Blockchain technology, often hailed as one of the most transformative innovations of the 21st century, is steadily gaining traction across the globe. In India, a nation known for its rapid adoption of cutting-edge technologies, blockchain is emerging as a game-changer in various sectors. From finance to supply chain management, healthcare to governance, the potential applications of blockchain are vast and varied. This blog delves into the significance of blockchain technology in India, its current state, and the promising future that lies ahead.

Understanding Blockchain Technology

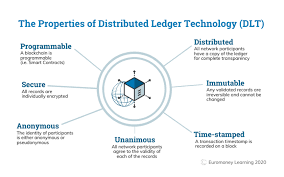

At its core, blockchain is a decentralized, distributed ledger technology that enables secure and transparent record-keeping. Unlike traditional databases managed by a central authority, blockchain operates on a peer-to-peer network where data is recorded in blocks and linked in a chain. Each block contains a timestamp, a cryptographic hash of the previous block, and transaction data, making it nearly impossible to alter or hack the information.

The Rise of Blockchain in India

India has been quick to recognize the potential of blockchain technology. The government’s push towards a Digital India and initiatives like Aadhaar have created a fertile ground for blockchain adoption. Various sectors are exploring the integration of blockchain to enhance transparency, reduce fraud, and streamline operations.

- Financial Services: The financial sector in India is one of the most significant beneficiaries of blockchain technology. With the advent of cryptocurrencies like Bitcoin and Ethereum, blockchain has already made its mark. Indian banks and financial institutions are leveraging blockchain to improve the efficiency of cross-border payments, reduce transaction costs, and enhance security. The Reserve Bank of India (RBI) is also exploring the possibility of a central bank digital currency (CBDC), which could further revolutionize the financial landscape.

- Supply Chain Management: Blockchain is poised to revolutionize supply chain management in India. By providing a transparent and immutable record of transactions, blockchain can help eliminate inefficiencies and fraud in the supply chain. Indian companies are increasingly adopting blockchain to track the movement of goods, verify the authenticity of products, and ensure compliance with regulations.

- Healthcare: In the healthcare sector, blockchain can play a crucial role in improving patient data management. With a decentralized ledger, healthcare providers can securely store and share patient records, ensuring privacy and data integrity. This can lead to better patient outcomes, reduced administrative costs, and a more efficient healthcare system. Several Indian startups are already working on blockchain-based solutions to address the challenges in healthcare.

- Governance and Public Services: Blockchain has the potential to transform governance and public services in India. By enabling secure and transparent voting systems, blockchain can help eliminate electoral fraud and increase voter trust. Additionally, blockchain can be used to manage land records, reduce corruption, and ensure the efficient delivery of public services. The Indian government is actively exploring the use of blockchain in various e-governance initiatives.

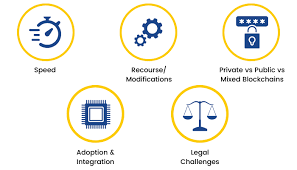

Challenges to Blockchain Adoption in India

While the potential of blockchain technology in India is immense, several challenges hinder its widespread adoption. These include:

- Regulatory Uncertainty: The regulatory landscape for blockchain and cryptocurrencies in India remains unclear. While the government has shown interest in blockchain technology, there is still ambiguity regarding the legal status of cryptocurrencies. This uncertainty has created a cautious approach among businesses and investors.

- Lack of Awareness and Expertise: Despite the growing interest in blockchain, there is still a lack of awareness and understanding of the technology among businesses and the general public. Moreover, the shortage of skilled blockchain professionals poses a significant challenge to its implementation.

- Scalability Issues: Blockchain technology, in its current form, faces scalability challenges. As the number of transactions increases, the network can become slow and inefficient. Addressing these scalability issues is crucial for the widespread adoption of blockchain in India.

The Road Ahead

Despite the challenges, the future of blockchain technology in India looks promising. The government’s proactive approach, coupled with the private sector’s enthusiasm, is driving the adoption of blockchain across various industries. As the technology matures and the regulatory landscape becomes clearer, we can expect to see a surge in blockchain applications in India.

India’s vibrant startup ecosystem is also playing a pivotal role in advancing blockchain technology. Numerous startups are working on innovative blockchain solutions that can address the unique challenges faced by the country. From financial inclusion to supply chain transparency, these startups are paving the way for a blockchain-powered India.

Conclusion

Blockchain technology holds the potential to reshape India’s economic and social landscape. As the country continues its journey towards digital transformation, blockchain will undoubtedly play a crucial role in driving transparency, efficiency, and innovation. While challenges remain, the opportunities presented by blockchain technology are too significant to ignore. With the right regulatory framework, investment in education and skills, and continued innovation, India is well-positioned to become a global leader in blockchain technology. The future is decentralized, and India is ready to embrace it.

Leave a Reply